Welcome back thriving real estate endeavors to another amazing episode of the Raising Private Money Podcast with Jay Conner!

Today, we share with you the best tips on how to successfully navigate the ever-changing waves of the real estate market.

Jay Conner sits down with special guest and good friend, Chris Prefontaine, an expert in real estate investing with almost 30 years of experience.

They delve into the world of creative financing, private money lending, and finding success in a niche market.

Chris shares invaluable insights for finding success in real estate investing, including finding a niche that you love, learning from someone experienced in that niche, and staying focused on your niche for 3 to 7 years, avoiding distractions along the way. Jay and Chris discuss the importance of following these principles.

What makes this episode even more exciting is the discussion on private money lending. Chris and Jay both share their personal experiences and the benefits they’ve gained by borrowing money from individuals instead of traditional lenders. They highlight the importance of treating people well, delivering on promises, and attracting private money lenders through solid relationships.

Additionally, Chris dives deep into the world of creative financing and terms, sharing his expertise in structuring deals without traditional bank financing. He walks us through his own experiences with creative financing for condominium conversions before the 2008 financial crisis.

Chris and Jay both emphasize the significance of understanding creative financing and terms, and how teaching others about these concepts can attract lenders and investors.

So, if you’re interested in learning more, be sure to tune in to the podcast episode and gain valuable insights from Chris Prefontaine and Jay Conner.

Lastly, as a special bonus, Chris Prefontaine is offering two free books to our listeners. Simply visit www.wickedsmartbooks.com/jay1 to claim your freebies!

Remember, successful and sustainable real estate investing is all about finding your niche, building relationships, and understanding the power of creative financing.

So grab your surfboard and join us as we ride the waves of opportunity in the real estate market!

Timestamps:

00:01 – Attracting Private Money For Real Estate Deals Without Asking For It

03:44 – Jay Conner: We Are Not Borrowing Unsecured Money

09:07 – Owner Financing With Free And Clear Property Or Subject To Seller’s Mortgage.

11:30 – Shortage Of Inventory, But Motivated Sellers Exist.

16:42 – Leading With A Servant’s Heart In Business.

17:43 – Private Money And Creative Financing

20:29 – Chris Prefontaine’s two free books to our listeners. Simply visit https://www.WickedSmartBooks.com/Jay1 to claim your freebies!

23:38 – Approach The Seller And Have A Conversation With Their Needs In Mind.

24:33 – Market Goals Accomplished Through Premium Financing.

29:34 – Find The Niche You Love, Find A Coach Who Can Help You Through The Real Estate Cycle, And Then Don’t Be Blinded By The Next New Shiny Object That Comes Your Way.

Connect With Jay Conner:

Private Money Academy Conference:

https://www.JaysLiveEvent.com

Free Report:

https://www.jayconner.com/MoneyReport

Join the Private Money Academy:

https://www.JayConner.com/trial/

Have you read Jay’s new book: Where to Get The Money Now?

It is available FREE (all you pay is the shipping and handling) at https://www.JayConner.com/Book

What is Private Money? Real Estate Investing with Jay Conner

http://www.JayConner.com/MoneyPodcast

Jay Conner is a proven real estate investment leader. Without using his own money or credit, Jay maximizes creative methods to buy and sell properties with profits averaging $67,000 per deal.

#RealEstate #PrivateMoney #FlipYourHouse #RealEstateInvestor

YouTube Channel:

https://www.youtube.com/c/RealEstateInvestingWithJayConner

Apple Podcast:

https://podcasts.apple.com/us/podcast/private-money-academy-real-estate-investing-with-jay/id1377723034

Facebook:

https://www.facebook.com/jay.conner.marketing

Twitter:

https://twitter.com/JayConner01

Pinterest:

https://www.pinterest.com/JConner_PrivateMoneyAuthority

Building Wealth Through Real Estate: Insider Perspectives with Chris Prefontaine & Jay Conner

Jay Conner [00:00:01]:

Welcome to another amazing episode of Raising Private Money. On this podcast, this is where we talk about how to attract and raise Private Money for your real estate deals without ever asking for money. Well, today I have got a very good Fran an amazing guest that you’re going to enjoy. First of all, my guest has been in real estate now for almost 30 years. His Experience ranges from constructing new homes and owning a Realty Executive franchise to running his investments, commercial and residential. Well, my guest runs his own buying and selling house business with his family team, which purchases 2 to 5 properties monthly. So they’re in the trenches every single week, knowing what’s going on in the market today. In addition to that, he’s a 3-time best-selling author of Real Estate on Your Terms, The New Rules of Real Estate Investing, and Monica Sawyer’s Real Estate Investing for Women.

Jay Conner [00:01:01]:

And he’s the host of a very popular real estate podcast titled The Smart Real Estate Coach Podcast. In just a moment, you’re going to meet my guest and good friend, Chris Prefontaine right after this.

Narrator [00:01:17]:

If you’re a real estate investor and are wondering how to raise and leverage Private Money to make more profit on every deal, Then you’re in the right place. On Raising Private Money, we’ll speak with new and seasoned investors to dissect their deals and extract the best tips and strategies to help you get the money because the money comes first. Now here’s your host, Jay Conner.

Jay Conner [00:01:47]:

Well, hello, Chris, and welcome to the show.

Chris Prefontaine [00:01:50]:

Hey, Jay. Great to see you as always. Glad to be back.

Jay Conner [00:01:53]:

It is great to have you back, Chris. Every time we have you on the show, we get rave reviews. Everybody loves hearing your advice and wisdom. So what we’re gonna do here on the show, since it says raising Private Money, we’re gonna talk about Private Money first, your experience with that, Chris. And then we’re going to move over to, one of your top experts, and that is buying and selling properties and controlling properties by using creative financing and terms. So first, let’s start with Private Money. Just to make sure Our listeners know what we’re talking about. We’re not talking about hard money.

Jay Conner [00:02:32]:

We’re not talking about hard money lender brokers. When we say Private Money, we’re talking about borrowing money, getting individuals just like us to fund our deals, and investing in our deals, either by using their investment capital or their retirement funds. So, Chris, when where, and how did your Private Money journey and experience start?

Chris Prefontaine [00:03:00]:

Man, in some shape, form, or fashion, this would have been way pre-crash. So, late nineties, early 2000, by way of word-of-mouth. In other words, I remember, like, it was yesterday, my CPA, my attorney who sees all our deals saying, hey. I got this money sitting in an IRA or 401k, and I wanna put it to work. I mean, that’s how it started for me. I never was not in the study. I’m not an expert like you, Jay, but that’s how it started just by sort of chatting with people that I know. And, of course, when someone does well with you and does well with anyone, they’re gonna they’re gonna talk about it.

Chris Prefontaine [00:03:34]:

So that was my short journey. And to this day, as you know, we’re gonna talk about it later. I don’t go out and actively seek it. It usually finds me at this level.

Jay Conner [00:03:44]:

Sure. Well, you know, I was visiting with, a friend earlier today, and We were having a conversation, and they asked me. They said, well, Jay, how long has it been since you actively were, you know, teaching people about, you know, what Private Money is and how they can get high rates of return, saving, and security? I said, you know, it’s probably been about 10 years since I actively Was looking to, raise more Private Money because first of all, once we get Private Money, Then they don’t want it back when we cash them out. They want us to put it back to work. Right. And so I’ve just been using the same 1,000,000 dollars over and over and over again. And, of course, and I’m sure the same thing is for you, Chris, People get referred to us all the time from existing, you know, our private lenders that want to do business with us.

Jay Conner [00:04:40]:

Right?

Chris Prefontaine [00:04:41]:

Yeah. That’s what I meant. I mean, it just started with a circle of 2 or 3 people, and now I, if I had to, could pick up the phone and go, hey. I got this new deal. And so, yeah, usually, you treat people the right way, you do what you’re supposed to do, you do what you say you’re gonna do, and then the money finds you.

Jay Conner [00:04:55]:

Yeah. You know, one misconception that new real estate investors have is, first of all, who would loan me Private Money? And, you know, I’ve never done a deal, or who’s gonna loan me Private Money? Well, the answer to the question is, if you, as the borrower, don’t pay the private lender, the property does. And what that means is we’re not borrowing unsecured money. We’re backing all the notes that we do by the real estate, you know, that’s being purchased. And, I tell you, Chris, and I know you’ve heard me say before, I got into this world of Private Money because I had a need. I mean, the 1st 6 years I was in the business, I thought you had I didn’t know anything about creative financing. I didn’t know anything about terms. I’d never heard of it.

Jay Conner [00:05:47]:

I thought you just had to, get your deals funded from the bank down the street. Well, that’s what I did for the 1st 6 years from 2003 to 2009. And then in January 2009, I got cut off from the banks like the rest of the world would never notice. And so I had to learn a different, you know, a different way. And you know what? It was the biggest blessing in disguise in my business Because, in this world of Private Money, we make the rules. Like, we set the interest rate, we set the frequency of payments, and we structure the whole deal. You know, the old, traditional way of borrowing money. As you go to the bank, you get on your hands and knees, and you put your hands underneath your chin, And you say, please fund my deal.

Jay Conner [00:06:31]:

Please fund my deal. But, of course, in this world, it’s not that. You’re already approved. There is no application. No credit score plays into this. There’s no verification of income. What do we do? We put on our teacher hat, our Private Money teacher hat, And we teach people that we’ve got some kind of association with, what Private Money is, and what self-directed IRAs are. And so then They’re chasing us, and we’re not chasing them.

Jay Conner [00:07:00]:

So, in your world, Chris, have you raised Private Money for, commercial short deals single-family houses only, or all the all the above?

Chris Prefontaine [00:07:11]:

All the above when I was doing it actively. I remember doing those specifically for, condominium conversion projects where we bought, like, sick not huge, like, 6, 8, nothing more than 10 units, and then turned those into condominiums from an engineering, legal, and construction standpoint and borrowed the extra funds to do that. Did a lot of that before the, o eighth debacle. And you said blessing in disguise. I wrote it down, Jay when you said it because you couldn’t have convinced me during that away time frame, and you said 09. So right now, the window, For me, it went up 12, I think. But you couldn’t have convinced me that it was a good thing, but it was a great thing. Because as you alluded to, that’s why it’s why we’re doing what we’re doing now.

Chris Prefontaine [00:07:50]:

It’s why you’re doing what you’re doing. Right? So everything for a reason, I always say.

Jay Conner [00:07:55]:

Absolutely. So, Chris, Let’s move to, one of your expertise, and that is doing terms, doing creative financing. So For the person that’s never heard about terms, that’s never heard about creative financing, what does that mean at its most basic level?

Chris Prefontaine [00:08:17]:

The basic level would be because of what I went through in 0 8, not utilizing banks because my credit was in the toilet and I had no cash, so they weren’t financing me, and it means not putting up gobs of money. Maybe with some exceptions, we’ll talk about, ladies, small amounts of money, But no money of your own, no credit, and, no banks. That’s what it means in a sense, in essence.

Jay Conner [00:08:40]:

So in the world of terms and creative financing. Well, let me back up. In the world of Private Money, the private lender is doing the funding. Traditional borrowing the bank is doing the funding. You know, if someone’s borrowing money from a hard money lender, the hard money broker is doing the funding. In the world of creative financing and terms, who is the bank?

Chris Prefontaine [00:09:07]:

I’ll give you 2 answers because there’s advanced stuff, but 2 answers. 1 is we love owner financing so the seller is gonna be the bank when the property is free and clear in particular. The building I’m standing in today was bought with a free and clear seller, no mortgage, and they became the bank. So that’s 1. 2 is the reason I said 2 answers, when we buy a property subject to the seller’s mortgage staying in place, the financing stays in place with the more with, the company that originally provided that seller with the mortgage and they stay as the guarantor. We just bought the property. So those are my 2 favorites, and so there’s no outside financing involved, especially not that you’re gonna ever sign on or pledge your credit or asset swap.

Jay Conner [00:09:50]:

Yeah. Well, I can tell you why I love subject to deals right now.

Chris Prefontaine [00:09:55]:

Yeah.

Jay Conner [00:09:56]:

Because I saw a statistic by Jason Hartman. He, was our keynote speaker at my mastermind group meeting last week. And, he’s just a brilliant, smart real estate investor and an economist. And, he had the stats to show us. It’s like right at 90% of all the mortgages right now in the United States have and they had it broken down by category, have got less than a 4% interest rate. Because Everybody refused. You know, some of them are, you know, less than 3%. But 90% of them are less than 4%.

Jay Conner [00:10:37]:

And I’m going, man, you buy a subject to today, and you inherit you inherit an interest rate less than 4%. I tell you what, you buy a house subject to the existing note at less than 4%, I don’t ever wanna get rid of that house.

Chris Prefontaine [00:10:54]:

Right. That was spot on. Just this morning, Jay, I’m shaking my head. We had a student submit a deal. I said, well, send me the mortgage statement. 3.8%. So I don’t know about you, but I don’t think we’re gonna see those rates, maybe not, in my 10 years here.

Chris Prefontaine [00:11:10]:

I don’t know, but I don’t think real quickly. And so how cool would it be to learn how to do that like you and I just talked about? Even if you the listener say, well, maybe I’ll just learn it to buy my own house. That’s a big win. That’s a skill set you’ll never lose. So once you learn how to do that, you can go grab those 90% of those houses that have those awesome, awesome loans on them.

Jay Conner [00:11:30]:

Absolutely. And, you know, there’s a lot of truth when someone says, well, all those people, the the the reason, you know, peep the reason people aren’t buying houses well, number 1, there’s still a shortage of inventory. But number 2, you hear it said, Well, everybody that’s got those mortgages at 2.7% and 3.7%. They’re not going to get rid of those houses. They’re going to hang on to them. That’s true except for one thing. There always have been and there always will be motivated sellers of properties because, you know, distress comes along for all kinds of reasons. You know? Ever since Adam and Eve, people have been dying.

Jay Conner [00:12:15]:

And there are inherited properties.

Chris Prefontaine [00:12:17]:

Yep.

Jay Conner [00:12:18]:

And those inherited properties, yes, a lot of them are free and clear. Well, as you just said, you can use your seller financing strategy on that. But for all those inherited properties that come with a mortgage, There’s a 90% chance it’s got less than 4%. So even though you hear in the news people aren’t selling houses, whether or not selling houses unless they are distressed. What would your comment be about that, Chris?

Chris Prefontaine [00:12:45]:

Well, I get I just thought of another one while you were talking. This is big now. When COVID pushed all these values up. Right? I’m building a house in another state right now, and this is rampant. That is the tax assessment has been put sky-high. People are annoyed. People are up in arms. But guess what? They gotta sell.

Chris Prefontaine [00:13:02]:

A lot of them have to sell. Like, I’m hearing a time at the time from my subcontractors and other people, and they had rates that were just tremendously low. That’s one issue right there. 2nd homes. Forget so death a 100%. 2nd homes after COVID, people say, you know, the media’s screaming negative. I don’t agree with them, but they are, and they’re scaring sellers. The sellers are dumping 2nd homes and all kinds of crazy stuff.

Chris Prefontaine [00:13:26]:

And the buyer pool has because of interest rates, is a little bit more, it’s smaller. It’s shrinking. Well, unbeknownst to them, there are people like you and I that’ll gobble those up in a heartbeat. And so there’s a lot of properties out there. We could I could list we could keep going. A dozen reasons why People will sell those properties.

Jay Conner [00:13:43]:

Exactly. What’s your preferred exit strategy, or strategy When you buy a house on terms with creative financing, either the seller finances it if it’s free and clear, or you buy it, sort of, to the existing note. What’s your preferred exit strategy?

Chris Prefontaine [00:14:02]:

I like it still to this day, Jay, and we’ve refined it so much with my son handling the buyer side, and that is the rent-to-own program when done properly. Let me qualify that. I hear I’m sure you do podcast after podcast where people, perhaps even teaching this, but guests on on shows saying, yeah. You know, we exit rent to own, and we don’t really care if the buyers qualify because we just put another buyer in there and collect another Yeah. That may be fine legally, but morally and ethically, it’s not, in my opinion. So we deal with who? We deal with buyers, and this has been a major, major increase since COVID, who either one of 2 things. 1, they started their own business. They left the corporate world because of COVID.

Chris Prefontaine [00:14:42]:

They’ve got They had great paying 5, 6, maybe close to 7-figure incomes. So they have income. They had. They have four zero one k. They have a nest egg. They go to buy a house. They can’t get them a loan, but for the most part, with a very conventional aggressive rate because they need seasoning, 2 years. Those are great buyers for our rent-to-own program because they are gonna cash it out.

Chris Prefontaine [00:15:02]:

And the other buyers would be the people that sadly went through whatever hiccup personally that need credit, enhancements. So we still have a very, very low default rate even coming through COVID. We default, like, somewhere between 2 and 5. I’ll be conservative saying 2 10% default. The rest cash out. So we do set up a big win-win on those. Now the properties that we own sub 2, according to our earlier conversation, we wanna own those forever. So we’ll let the tenant-buyer who comes in on the rent-to-own program know that if they don’t default the payment and they get their down payment up to 20%, then we’ll owner-finance them.

Chris Prefontaine [00:15:37]:

They’ll never have to see a bank. And that’s pretty cool because we can be super competitive when we’re buying houses in the 2, 3, 4% range. We can still be competitive and profitable on the owner financing and do the buyers a big favor. So that’s our favorite, exit. And then Kinda tier 2 is owner finance them if we’re into that property for the long term.

Jay Conner [00:15:56]:

Yeah. I love, your outlook. I’ve got the same philosophy. My wife, Carol Joy, and I decided years ago when we started our rent-to-own program selling it, we said, look, we’re gonna do everything that we can to help these people own a house. Yeah. And I mean, as you say, I mean, it’s true. If you don’t help them, if you don’t hold their hand, if you don’t give them a plan, the likelihood of them ever, you know, getting ready for a mortgage is, you know, slim to none, and slim just got up and left. And, you know, a real estate entrepreneur or a real estate investor, when you know that that’s gonna be the case, you’re setting up your buyer for failure.

Chris Prefontaine [00:16:42]:

Yeah.

Jay Conner [00:16:42]:

And, you know, I wanna feel good about my business, and, you know, what I’m doing to lead with a servant’s heart. Everything we do and everything you do, Chris, we’re leading with a servant’s heart. How do we do that? Well, in the world of Private Money, I’m not asking, begging, or chasing. I’m teaching and serving these people. And up to we have just received countless thank you notes and thank you, you know, conversations from our private lenders about changing their retirement years. And the same thing applies to when, you know when you’re working with sellers. I mean, When a seller responds to our marketing and they’re in foreclosure, one of the first things we do is ask them, do you want to keep your property? And if they say yes, and we’re able to give them an idea, such about a loan modification or whatever, and they’re able but, you know, I believe in the law of reciprocity, and what goes around comes around. As Zig Ziglar says, if we help enough other people, you know, get what they need and want.

Jay Conner [00:17:43]:

We don’t have to worry about ourselves. And then again, the same thing applies to the terms. Chris, I have a question for you. My general rule of thumb and there are always exceptions, there are always exceptions, but my general rule of thumb is if I pay all cash for a property with Private Money. And, you know, some people won’t sell on terms. I’m thinking about 411 Chatham Street right now. A free and clear house negotiated to buy with seller financing after a repaired value of $240,000 I’m only into, like, 30,000 in rehab. He said I want all cash, $90,000.

Jay Conner [00:18:22]:

And it, you know, didn’t have any floor covering. It didn’t need some rehab. Well, I gave him multiple offers. I said I’ll pay you all cash 90,000. Or if you want, I’ll pay you $120,000 and, you know, pay him $30,000 more by giving him monthly payments. Well, The answer was no. All cash or no deal. So anyway, we paid all cash in that case.

Jay Conner [00:18:49]:

So anyway, my rule of thumb typically is if I’m using Private Money to fund the deal, if I’m paying all cash, I’m typically going to want to cash out. But if I’m buying on terms with creative financing, I’m typically gonna want to sell on terms, rent to own, etcetera. Do you agree with that philosophy?

Chris Prefontaine [00:19:11]:

Oh, yeah. A 100%. Give you an example. When we buy on a franchise, remember I said earlier that I prefer free and clear. Well, 99%, almost all of those deals we do with very few exceptions, and we can talk around if we have time, are done principal-only payments. So, like, we bought a this isn’t just for low-end homes. We bought a house in the water. Cape Cod, it’s a resort area not too far from here.

Chris Prefontaine [00:19:33]:

945,000, just under 1,000,000 on the water. Kicker. The seller is a realtor who couldn’t sell it. She’s a Boston realtor. We structured that deal, 945,000 purchase. Restructured $25100 monthly principal-only payments. Why would I ever wanna cash out of that deal when I have 30,000 a year coming to write off a principal regardless of what I do with the house? And and punchline, the the buyer in that house waiting to get qualified is paying it every month, paying us with a spread on top of it.

Chris Prefontaine [00:20:04]:

So, yes, the short answer is, of course, I wanna stay in the deals. And then the sub-two deals where there is no time ticker. You know? There are no terms. There’s no balloon. I wanna say no’s forever. I hope I hope my grandkids have those houses because that’s it’s just a piggy bank. We trademark what we call the 3 payday system. I feel like when we stay in the deal and we own finance, it’s like creating a 4th payday that goes on for life, potentially, if you want it that long.

Jay Conner [00:20:28]:

I love it. Just in case, any of our listeners need to hop off early before we finish, I know you’ve got a gift for, all of our listeners. You wanna wanna go ahead and share that gift with them, Chris?

Chris Prefontaine [00:20:40]:

Yeah. They’re gonna get and and I wanna I wanna just disclosure here. This is not one of those gifts that you gotta get through the funnel and then you gotta pay for shipping. Alright? We give you the books for free. We’re gonna send you a couple, we have, 4 now. We’re gonna send you 2 of our best-selling books, real estate on your terms and deal structure over time. I might throw in some other goodies in there for you. Just go to www.WickedSmartBooks.com/Jay1.

Jay Conner [00:21:10]:

Alright. So again, nice and slow. Let everybody know what that URL website is.

Chris Prefontaine [00:21:16]:

www.WickedSmartBooks.com/Jay1.

Jay Conner [00:21:26]:

Awesome. Now terms, Can you only, can you only buy properties or only single-family houses on terms? Or what kind of asset classes can you structure with, terms?

Chris Prefontaine [00:21:42]:

Yeah. I love this, Jay, because since literally 1600, this has been done. You could buy any asset class, and as you know, people buy boats and cars and all kinds of things on terms. This office building I’m standing in was bought on terms. We’ve done multiple terms. I love, being out there doing all kinds of asset classes. However, the reason people say, well, why do you teach primarily single families? Because if I ever got into a room and started teaching you can do all this stuff, the shiny object syndrome kicks in. Right? Oh, I wanna get one of those buildings.

Chris Prefontaine [00:22:12]:

I wanna get no. You then you’ll never have a business. So we start with singles, and when you know the skill set, no one can take it from you. You can buy anything you want. You can go target things you want. We target If you want an office building, I sold this one. I sold this one last month. So I’m targeting ZIP codes to buy another one for you and Claire and do the same thing again.

Chris Prefontaine [00:22:30]:

It’s that simple.

Jay Conner [00:22:32]:

So any asset class can be negotiated on terms.

Chris Prefontaine [00:22:36]:

Yep.

Jay Conner [00:22:37]:

So, I know we’ve only got about 7 and a half minutes left. So I wanna ask you to answer a 3-day seminar in 7 minutes or less. Okay. I think that’s in the name of

Chris Prefontaine [00:22:52]:

Raymond, Jay. I can do it quick.

Jay Conner [00:22:54]:

A 3-day seminar question. So what are some of the most valuable, tips strategies, and advice you can give on how to negotiate with a seller? So this is gonna be a wide-open question, so you go with it the way you want to.

Chris Prefontaine [00:23:11]:

Sure.

Jay Conner [00:23:12]:

What are some tips and strategies from your years of experience that, would be helpful when we are negotiating with a seller of a property? And what is it about your offer and your talk off and your conversation that would convince them to take your seller-financed offer?

Chris Prefontaine [00:23:35]:

Yep.

Jay Conner [00:23:36]:

Over and beyond cash.

Chris Prefontaine [00:23:38]:

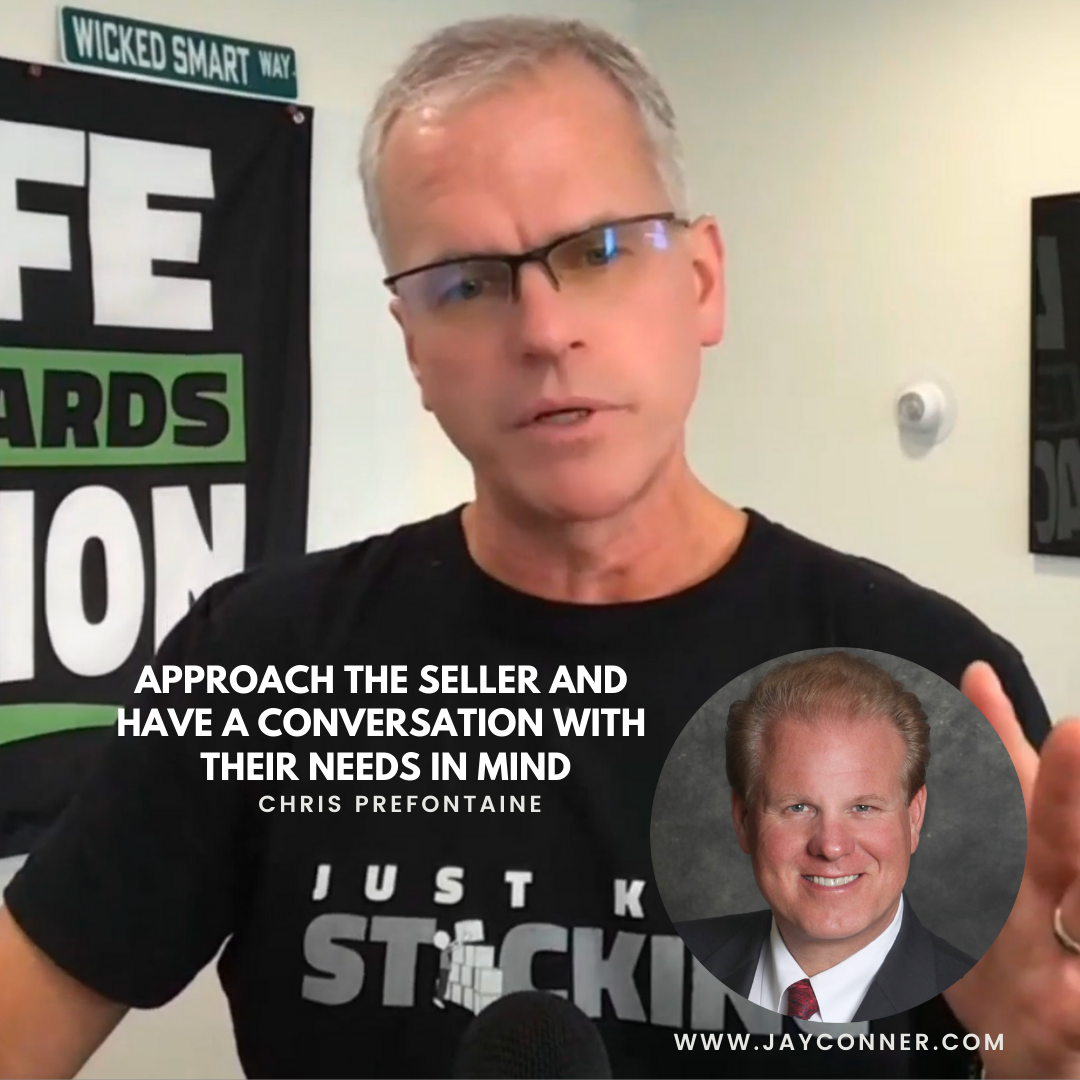

Yeah. This is key. I just got from Mastermind saying this to one of my higher-level groups. When you approach a seller conversation with 1 thing maybe 2 things in mind, you will always come out of that feeling good in either a deal or not, but it’s okay. And here’s why I say that. When you approach the conversation, how can I help the seller? What is one of 2 things? What is the problem they’re trying to solve that the market’s not solving or what goal are they trying to accomplish that the market’s not providing?

Chris Prefontaine [00:24:09]:

So two quick examples, divorced couple, not too far from here. One’s on the mortgage, one’s on the deed. The problem they were trying to solve was that they ran out of rehab money, and financing on credit cards, and we were in arrears 2 months. The problem they need to solve, they need the arrears caught up or they’re going into foreclosure. And because of divorce, they don’t wanna live there anymore. They want closure in the house, period. So we bought that sub-two. So we solved a problem.

Chris Prefontaine [00:24:33]:

On the other side of the coin, if someone’s free and clear like this building, are we trying to solve a problem? Usually not. Usually, it’s to try and accomplish a goal the market’s not providing, and that is full price, even a premium price. We paid a slight premium on this one. And what were they trying to do on top of that? Tax planning and estate planning. Sadly, I think he knew this gentleman passed away after a few years of being solid financing, but he provided his wife and his son a cash flow stream, not a building. Right? So we provided him with a solution to his goal the market was not giving him our financing. And, on the couple side, we fixed a major headache. So if you can do one of those 2 things now if you can’t, it’s okay.

Chris Prefontaine [00:25:14]:

No, Chris. I need the cash tomorrow to go buy my family a house in this particular area, and there’s nothing you can say about that’s gonna change my mind, And it doesn’t matter if I take less. Okay. I’m not your buyer. If something changes, I’m your plan b. That’s it. And don’t be attached to it. Look for people that you can help.

Jay Conner [00:25:32]:

I love it. There’s the philosophy again. Leading with a servant’s heart, looking to help, looking to solve their problem, which is their pain. Helping them get out of pain, whether that’s financial pain or emotional pain. So when you are negotiating with a seller and they have a mortgage. The first thing we think about is the subject-to. Buying it is subject-to. Well, you know what the monthly payment is going to be because that’s already established by the current mortgage that’s in place.

Jay Conner [00:26:02]:

So we know what the underlying debt is. We know what the monthly payment is. However, on the others, on, in another case for seller financing, It’s free and clear. There is no mortgage, so you’re gonna be creating a new mortgage. What advice would you give on how do you go about establishing, and offering a monthly payment, or you might start by asking getting a number out of them what’s the least they could take per month. So how does the conversation go on negotiating a monthly payment, no down payment, or a down payment?

Chris Prefontaine [00:26:37]:

I’m usually gonna start with, I tell them either 3 variables and I tell them to picture a seesaw, or if they’re bringing up other variables like interest rate down. You know, to bring up a lot, I’ll use a quadrant. Either way, the conversation goes like this. They say, well, I need a down payment or I need this price. I say, right. Listen, Jay. I have a few variables that you and I have to work on. I obviously can’t give you all of them.

Chris Prefontaine [00:26:59]:

That wouldn’t be fair. So we’ve got a price, We’ve got the term, the length, and we’ve got monthly. Now if they bring up something else like interest rate or or whatever, I’ll add it. I’ll add the 4. But I’ll say, which 1, number 1 in that list of 3 or 4 is most important to you, and then what’s 2nd most important? And then I’ll go back and work on that, and I’ll make sure. Because sometimes we jump the gun and get nervous about no down or get nervous about price when they didn’t need that or want that. So just find out what variable out of those 3 or 4 is most important to them and then solve for that.

Chris Prefontaine [00:27:31]:

Now in the meantime, what do I wanna make sure I do? If they’re free and clear, I know in my head I’m going out to the rent-to-own market. If I’m going out to the rent-to-own market, I have to be cognizant of what the rates are today that my buyer is gonna be looking at this house and saying, well, I’m gonna be at this amount eventually. I have to be below that to make any spread every month, which is what we call our payday too. So I’m gonna be cognizant of that as I’m talking to them. I’m gonna first find out what’s most important on their list of, on the pecking order.

Jay Conner [00:27:59]:

So, again, repeat those initial 3 variables.

Chris Prefontaine [00:28:03]:

And get them

Jay Conner [00:28:04]:

if you get them to prioritize.

Chris Prefontaine [00:28:06]:

Yeah. If they don’t bring up anything else, I wanna focus them on price, length of term, and monthly payment, these are free and clear people. If they don’t bring it up for anything else, those are the 3 I want them to prioritize for me.

Jay Conner [00:28:17]:

Awesome. And the down payment was not in there. Right?

Chris Prefontaine [00:28:20]:

Correct. Because they didn’t bring it up yet. If they bring it up, here’s the script. I’ll give you a script. If they bring it up, I say, Jay, the sellers I buy from typically because this this this works on their ego, this script. It’s it’s just brilliant. Most of the sellers I buy from prefer top dollar versus a small down payment. They usually don’t need the money.

Chris Prefontaine [00:28:41]:

And the response I get from a seller is, well, I don’t need the money. Okay? Great. So we take that out and say, well, we should work on these other 3 variables. It’s magical when you use that script.

Jay Conner [00:28:51]:

I love it. I love it. Most of the buyers I buy from today are more interested in, the top dollar price versus the down payment because they don’t need the money.

Chris Prefontaine [00:29:02]:

Well, and I word I use the word small. Versus a small down payment, like you’re belittling them, You don’t need that small amount of money. You want the price.

Jay Conner [00:29:11]:

I love it. That is a brilliant script. One more time, Chris, give out the URL for the gifts that you and your team are gonna ship out.

Chris Prefontaine [00:29:21]:

Sure. www.WickedSmartBooks.com/Jay1.

Jay Conner [00:29:28]:

That is awesome. Chris, it is always a blast to have you come here on Raising Private Money. And, final parting words and advice as we close out.

Chris Prefontaine [00:29:39]:

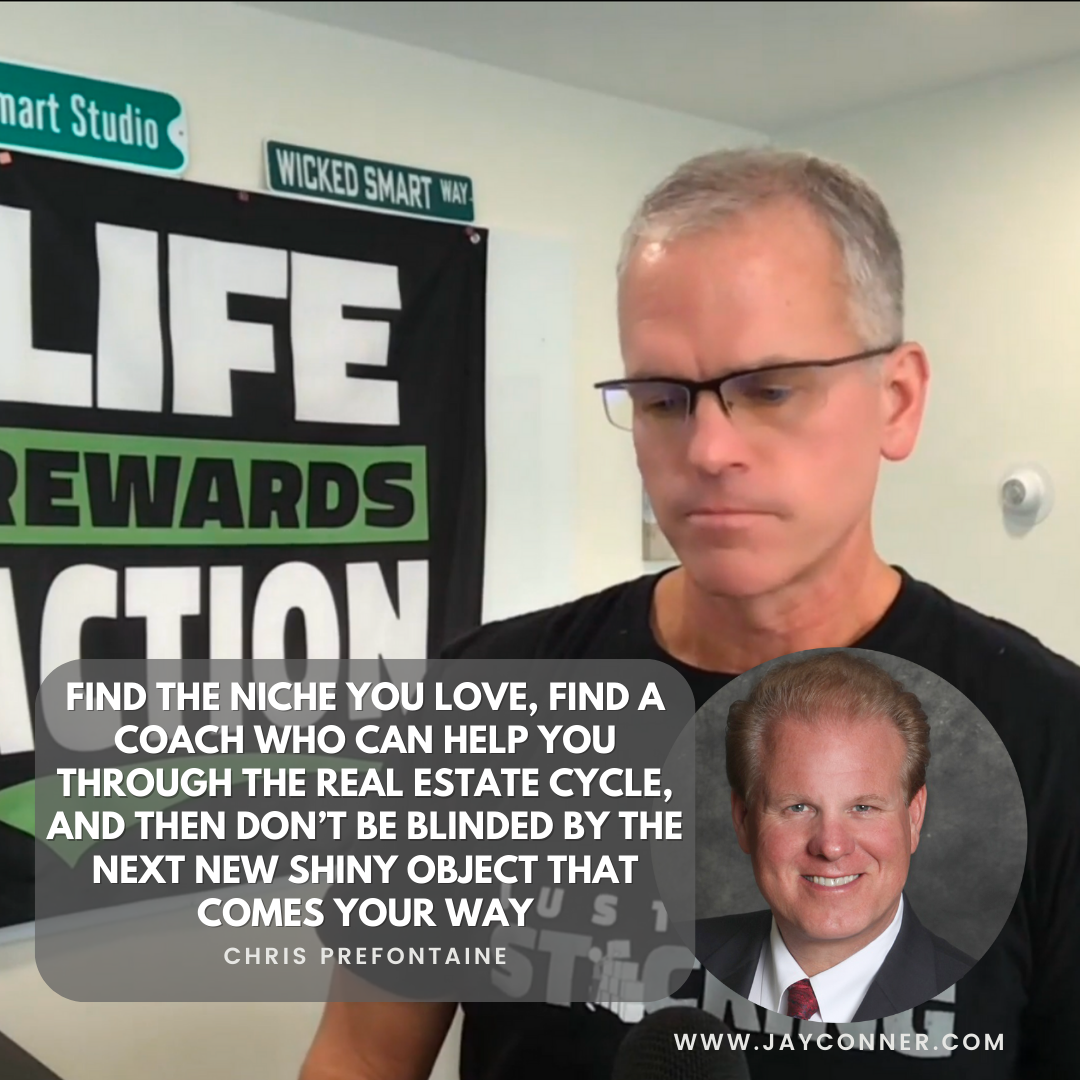

Yeah. Because you and I love teaching, I’m not so naive to think that, Either one of us has the the best niche. Right? They’re all awesome niches. So here are 3 quick tips. Find a niche that you can get behind that you love. Find someone in that niche like Jay or myself that had been through a bunch of cycles, and then put the blinders on for 3 to 7 years, and you’ll have a great experience. Don’t get caught up in the shiny object syndrome.

Jay Conner [00:30:01]:

Awesome advice, Chris. Thank you so much for joining us here on Raising Private Money.

Chris Prefontaine [00:30:06]:

Thank you, buddy.

Jay Conner [00:30:07]:

You got it. And there you have it, another amazing episode of Raising Private Money. I’m Jay Conner, the Private Money Authority, and I wish you all the best. And we appreciate the subscribers. Ring that bell if you’re watching on YouTube so you don’t miss out on future episodes. And if you happen to be listening on, iTunes or on Spotify, be sure and follow me. We look forward to seeing you right here on the next episode of Raising Private Money.

Narrator[00:30:36]:

Are you feeling inspired by the knowledge you gained in this episode? Then head over to www.JayConner.com/MoneyGuide. That’s www.JayConner.com/MoneyGuide and download your free guide that shares 7 Reasons Why Private Money Will Skyrocket Your Real Estate Investing Business Right Now. Again, that’s www.JayConner.com/MoneyGuide to get your free guide. We’ll see you next time on Raising Private Money with Jay Conner.